According to 2024 research, card payments dominate the Nordic countries’ payment landscape, with 90 percent of shoppers using them for contactless payments either daily or once a week. This success stems from strong government support and extensive digital payment infrastructure and results in the Nordic region being at the forefront of a new banking software development phenomenon – neobanks with a strong emphasis on technology, innovation, and customer-centric services.

What Are Neobanks?

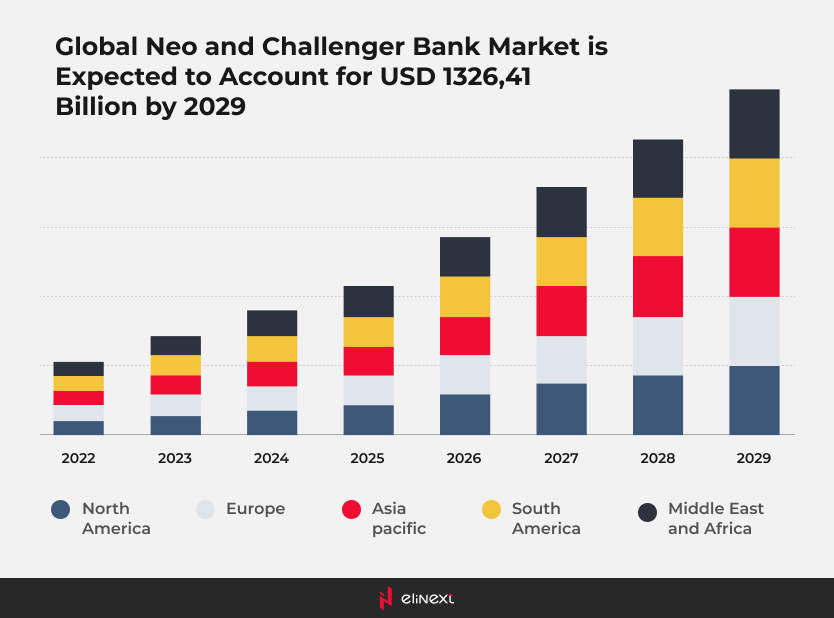

In practical terms, different types of neobanks, aka digital-only banks, refer to financial services providers that operate entirely online, without traditional physical branches, and often focus exclusively on a mobile app for their services. Global transactions of neobanks are projected to exceed $9 trillion by 2027, tripling from 2022 levels, with the number of users expected to double during the same timeframe.

What Are Challenger Banks?

Challenger banks are modern financial entities designed to rival traditional banks by delivering innovative and customer-focused services mainly through digital channels. These banks usually function without physical branches, utilizing technology to ensure a smooth and efficient banking experience for their users. As for challenger banks vs. neobanks, many neobanks evolve into challenger banks as the latter provide a wider range of services and rely on a banking license for that.

5 Types of Neobanks Redefining the Nordic Financial Services Industry

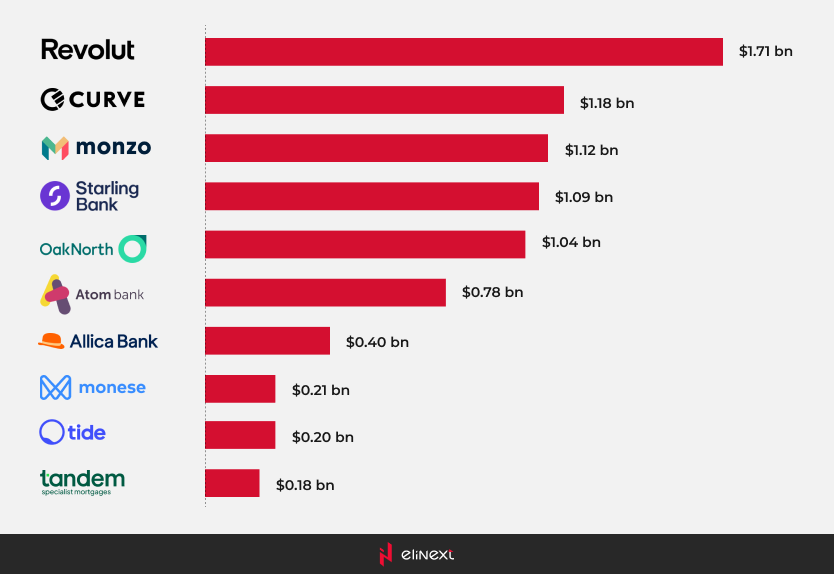

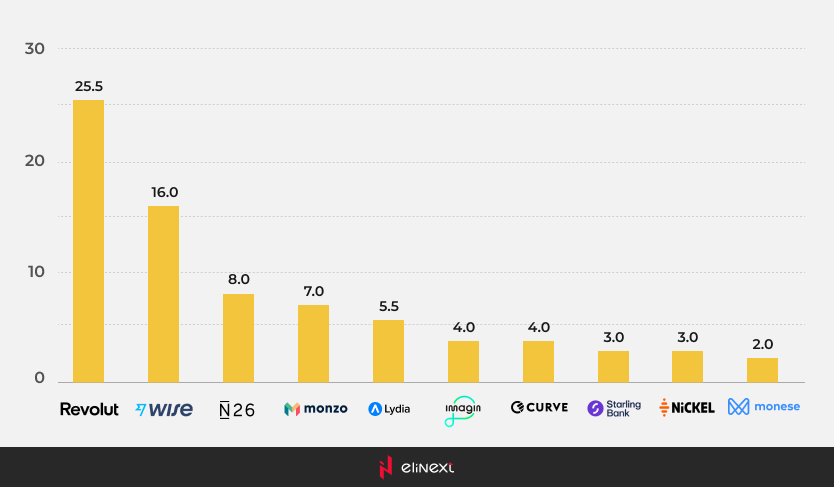

Revolut (United Kingdom)

Revolut began as a foreign exchange card aimed at travellers frustrated by high banking fees. It has since evolved into a comprehensive financial super app, offering multi-currency accounts, cryptocurrency trading, stock investments, budgeting tools, and business banking. As of 2025, Revolut serves over 30 million customers across 35 countries, with a strong presence in Europe, the U.S., Australia, and Asia, catering to diverse demographics, including millennials and SMEs.

Lunar (Denmark)

Founded in 2015, Lunar, a fully digital mobile banking app, serves both individual and business customers, offering services like insurance, savings, budgets, loans, and investments. Lunar Business, a part of Lunar, supports small businesses with a comprehensive package, while junior accounts for ages 15-17 provide basic functions. Lunar has over 950,000 customers across the Nordics and was last valued at approximately $2.2 billion. In late 2024, Lunar separated its Banking-as-a-Service (BaaS) business into a distinct entity, claiming that its revenues can compete with those of its core bank.

Rocker (Sweden)

Rocker AB is a Stockholm-based fintech company aiming to create the best platform for everyday financial services and sustainable payments. Its business area provides savings, payments, loans, and credits through the Rocker app. The Rocker Pay segment facilitates secure and flexible transactions for individuals trading in used goods. Rocker is licensed as a payment institution in Sweden regulated by the Swedish Financial Supervisory Authority. In February 2022, Rocker achieved a remarkable milestone by being the first challenger bank in the Nordics to launch a full-scale biometric card, Rocker Touch.

Holvi (Finland)

Holvi, a pioneering Finnish neobank, is designed for freelancers, entrepreneurs, and small business owners, focusing on simplifying financial management by merging banking and business tools into an intuitive platform. It stands out with unique features like integrated invoicing for cash flow management, automatic expense tracking for better visibility, customizable business accounts, tax reporting tools, a Holvi Business Mastercard for seamless transactions, and transparent pricing with no hidden fees. As of 2025, Holvi operates ca. 200,000 customers in Finland, Germany, and Austria.

Wise (United Kingdom)

Wise, formely TransferWise, specializes in international money transfers, offering competitive exchange rates and multi-currency accounts. As of 2025, Wise serves over 16 million customers worldwide, including individuals, freelancers, and businesses, processing more than £10 billion in transactions each month. The platform operates in over 70 countries and facilitates transfers to and from more than 170 countries, with significant markets in Europe, North America, and Asia-Pacific.

The Difference Between Neobanks and Challenger Banks

Neobanks vs. challenger banks differ mainly in licensing and services. Neobanks operate online without a banking license, offering basic services like current accounts to small businesses, relying on partner banks. Challenger banks, however, have a banking license, allowing them to provide a wider range of services, including loans and credit cards, targeting underserved consumers. An important note about challenger banks vs. neobanks would be that all challenger banks started as neobanks.

What are the future trends for digital banking in the Nordics?

The phenomenon of challenger banks vs. neobanks has sparked competition, pushing traditional banks to improve strategies and customer experiences. These digital players offer streamlined interfaces, personalized services, and quick responses, driving innovation and enhancing user experience. The neobanks vs. challenger banks rivalry will continue while technology won’t write off neobanks vs. traditional banks issue.

Integration of AI and automation in banking services

Integration of Machine Learning solutions and automation into banking services has demonstrable financial benefits and is likely to reshape the industry further. Thus, JPMC reports AI solutions has cut fraud by enhancing payment validation, reducing account validation rejections by 20%, and achieving notable cost savings.

Partnerships between FinTech and traditional banks

Adoption of financial software development services is a key to evolution of traditional banks towards a customer-centric approach. Fintech-bank partnerships blend fintechs’ user-friendly, digital solutions with banks’ trust, and drive financial inclusion, streamline processes with AI, cut costs, and unlock new revenue by combining agility with established infrastructure.

Expansion of crypto and blockchain-based financial services

The rise of crypto and blockchain development solutions is transforming finance with secure, decentralized solutions. Services like cross-border payments, smart contracts, and decentralized finance (DeFi) offer speed, transparency, and lower costs. Blockchain also enhances fraud prevention and accessibility, empowering global financial inclusion.

Regulatory scrutiny on digital-only banks

Regulators are focusing on prevention of money laundering, sanctions compliance, and counter-terrorist financing, increasing scrutiny on challenger banks. Concerns over vulnerabilities in neobanks have grown, pushing them to rethink processes and match the compliance standards of traditional banks.

Conclusion

The rapid advance of technology and shifting consumer demands have brought neobanks vs. traditional banks issue on the banking agenda. While the benefits of neobanks are extensive, this transformation highlights the critical role of regulation and collaboration in driving innovation. Collaborative strategies, like partnerships with fintechs and traditional banks, can help address scalability challenges and navigate regulatory hurdles effectively, ultimately resulting in a balanced, forward-looking financial ecosystem.

Planning to join the Nordic fintech community with an innovative solution? Elinext is poised and ready to help you pave the way.

As a trusted fintech software development services company with 30-year expertise, Elinext can help you launch, grow or upgrade your product, whether you’re a young startup or a mature brand looking to explore new opportunities.

Our ability to create tailored experiences, adapt to evolving client wants and needs, and stay agile has been instrumental in the successful delivery of multiple challenging fintech projects, including Financial risk management software, 3-tier ERP and payment processing solution, Software for processing and management of securities for a global fintech company, and more.

One of our recent ambitious projects, the Update of UK-based Crypto Digital Bank, stands out with its particularly successful outcomes.

Despite an extremely tight deadline, the development team managed to complete the project on time. The well-coordinated joint efforts of our vetted experts have resulted in improved app performance and balanced usability. Moreover, the new value-added features have increased the active user base significantly and helped to achieve deeper market penetration.

FAQ

What is the difference between neobanks and challenger banks?

The principal issue around neobanks vs. challenger banks lies in the availability of a banking license: neobanks operate fully online without a banking license, relying on partner banks for services, while challenger banks are licensed and offer broader services.

What are the key benefits of neobanks?

Key benefits of neobanks include lower fees, easy access, user-friendly digital-first services, and innovative products. E.g., neobanks stand out due to reduced overhead costs, unlike traditional banks that require higher admin fees for branch networks.

What are the benefits of challenger banks?

Comparing challenger banks vs. neobanks, it is worth mentioning that all license available with the former enables challenger banks to provide a comprehensive suite of financial services, instilling greater trust through regulatory compliance and financial protections, as well as allowing for scalability and longevity through independent operations.

How do traditional banks respond to neobanks and challenger banks?

Traditional banks adopt advanced technologies to enhance customer experience and efficiency while leveraging physical branches to offer a hybrid model neobanks and challenger banks cannot replicate. Traditional banks also leverage their reputation, bundled services, and in-person convenience – factors that keep many consumers loyal to legacy institutions.